According to customs statistics, the total import and export value of China's goods trade in the first two months of 2025 was 6.54 trillion yuan, a year-on-year decrease of 1.2%. Due to a decrease of 2 working days in the first two months of this year compared to the same period last year, after excluding incomparable factors, the actual growth of imports and exports was 1.7%. Among them, exports amounted to 3.88 trillion yuan, an increase of 3.4%; Imports amounted to 2.66 trillion yuan, a decrease of 7.3%. Measured in US dollars, the total import and export value for the first two months was 909.37 billion US dollars, a decrease of 2.4%. Among them, exports amounted to 539.94 billion US dollars, an increase of 2.3%; Imports amounted to 369.43 billion US dollars, a decrease of 8.4%.

In terms of specific products, China's integrated circuit exports reached 180.44 billion yuan in the first two months of 2025, a year-on-year increase of 13.2%. In terms of imports, the import value of mechanical and electrical products was 1 trillion yuan, an increase of 3.2%. Among them, the import volume of integrated circuits was 83.46 billion, an increase of 6.3%, and the import value was 402.28 billion yuan, an increase of 3.9%; The import volume of automobiles was 56000 units, a decrease of 45.8%, and the import value was 21.6 billion yuan, a decrease of 49.7%.

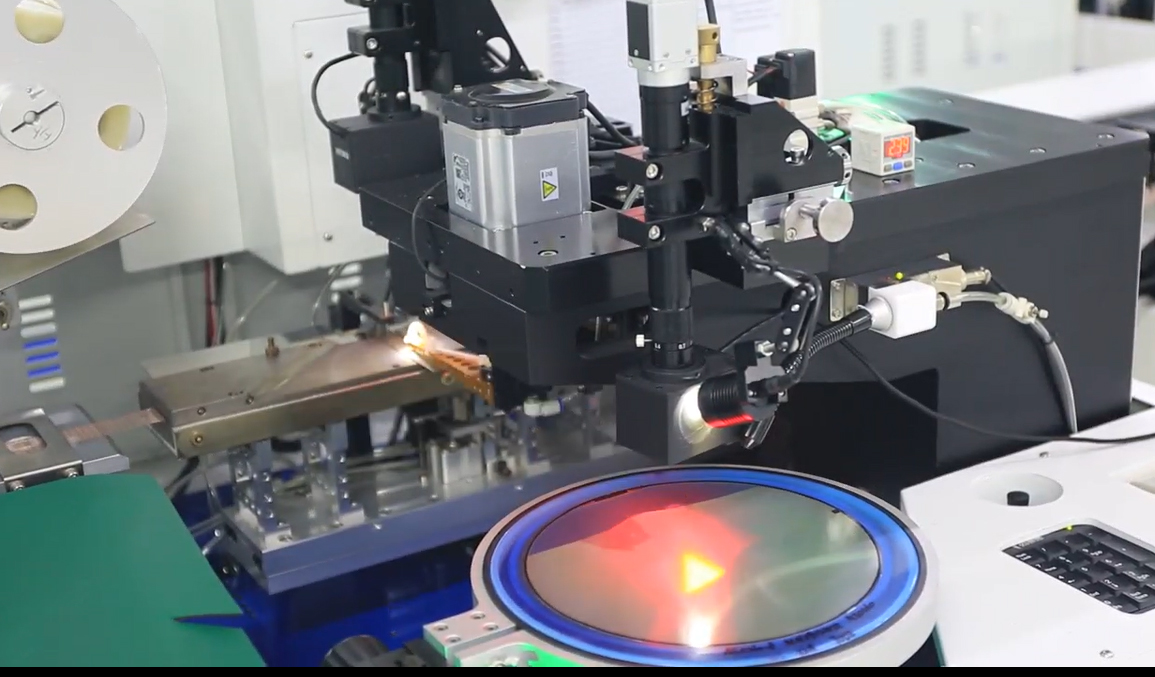

According to a research report by Guolian Securities, the Chinese semiconductor market accounts for about 30% of the global semiconductor market. Chinese companies are investing heavily in traditional chip manufacturing, which coincides with the imminent recovery of the global chip industry (mature processes such as 28nm). According to institutional statistics, in 2023, the capacity of semiconductor manufacturers in Chinese Mainland will increase by 12% year on year, reaching 7.6 million wafers per month. It is estimated that by 2024, chip manufacturers in Chinese Mainland will add 18 projects, with a 13% year-on-year increase in capacity, reaching 8.6 million wafers per month.

However, as the United States and other countries implement export controls on advanced equipment, enterprises in Chinese Mainland have instead expanded their investment in mature processes (28nm and more mature processes). It is estimated that by 2027, the mature manufacturing capacity in Chinese Mainland will account for 39%.

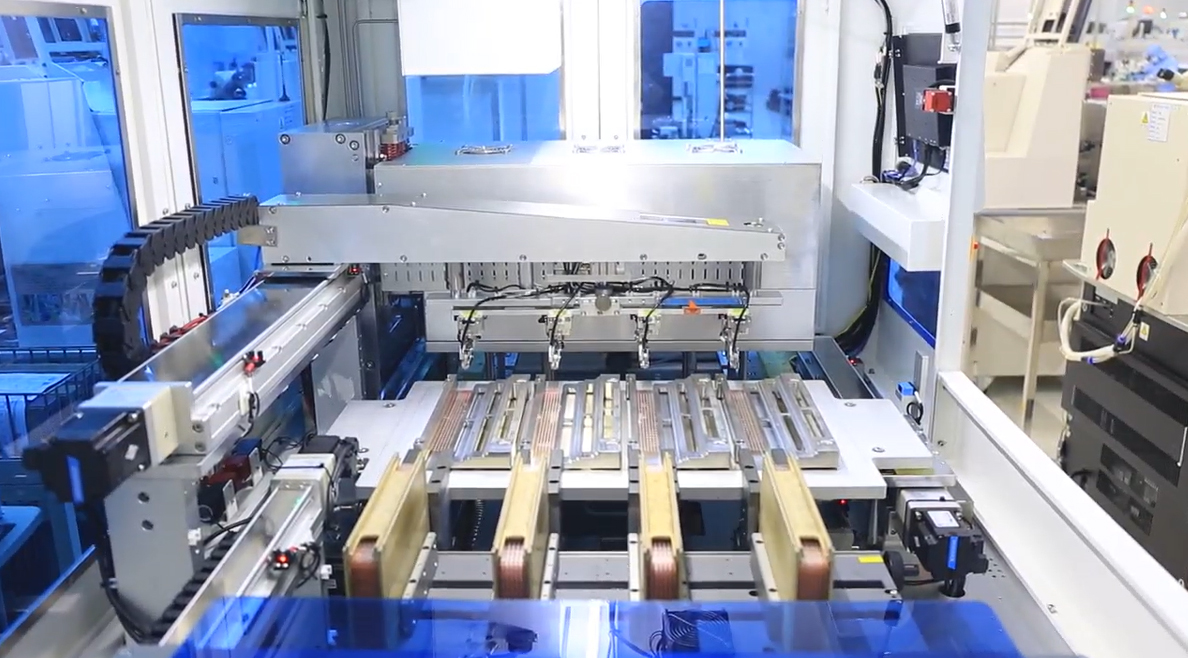

With the increasingly fierce competition in the global semiconductor industry, China is gradually emerging in the fields of mature process chip manufacturing and silicon wafer production, which has a profound impact on the global market. Traditionally, mature process nodes (i.e. nodes larger than 20nm) have been the main advantage for non cutting-edge chip manufacturers, providing support for fields such as consumer electronics and automotive electronics, and providing valuable profit sources for the entire chip industry's research and development departments. However, with China's rapid rise, especially in silicon wafer manufacturing, Western semiconductor companies are facing unprecedented pressure.

In the past, the production of mature process node chips was mainly dominated by some traditional large semiconductor companies, such as Intel, Texas Instruments (TI) in the United States, and Renesas Electronics in Japan. These companies rely on mature process technologies (usually nodes of 28nm and above) to provide a large number of chip products for multiple fields such as household appliances, automobiles, and industrial equipment.

Despite China's strong growth momentum in traditional process node chip production, there is also a potential market risk - oversupply. IDC analysts pointed out that with the large-scale expansion of Chinese enterprises, there has been an oversupply of mature node chips, which has affected the market's supply-demand balance. Many Chinese companies overly rely on the local market, which may lead to overcapacity and trigger a vicious cycle of price wars.

In addition, as the number of Chinese wafer fabs continues to increase, Western companies will have to face increasingly fierce market competition. The price decline will directly affect the profit level of these enterprises. In this situation, Western companies are likely to increase their investment in innovation and seek technological breakthroughs to maintain competitiveness, but this requires significant funding and time investment, making it difficult to quickly reverse the situation in the short term.

CN

CN EN

EN